Mortgage Rates Today: What the Data Says

Okay, let's dissect this mortgage rate situation. The headlines are screaming about the "lowest rate of 2025," tying a previous low in October at 6.06% for a 30-year fixed. Zillow's data is the primary source being cited. But before we break out the champagne, a few grains of salt are required.

Rate Reality Check

First, we need to understand the context. We're nearing the end of November 2025. Multiple sources mention the Fed's rate cuts earlier in the year and the possibility of another cut in December. The market is clearly anticipating this, which is already baked into current rates. The question isn't whether rates are "low," but whether they're likely to stay low or if this is a temporary blip.

Optimal Blue's data, cited by Fortune, paints a slightly different picture. Their average for a 30-year conventional mortgage is 6.224% as of November 21st. That's a discrepancy of about 16 basis points compared to Zillow’s 6.06%. Which number is "right?" Both are likely accurate samples but reflect different data sets and methodologies. (It's crucial to remember that these are national averages; your mileage will vary wildly based on credit score, down payment, and location.)

Then there's the NerdWallet report, which indicates a jump up to 6.09% APR. This volatility highlights the fundamental issue: daily tracking is mostly noise. Focusing on the month-long trend, as NerdWallet suggests, is far more useful.

The deeper problem is the reliance on short-term fluctuations. As one source notes, rates have been "hovering around 7%" for what feels like an eternity. The brief dip after the Fed's September meeting quickly reversed. The article mentions that in January 2025, the average 30-year fixed rate exceeded 7% for the first time since May of the previous year. Now, we're supposed to be excited about 6.06%?

The "Trending Mortgage Rates" article provides a longer-term perspective. It points out that rising rates began in 2013 and are expected to continue for another two decades. The author also notes that government interference in the economy is adversely affecting homebuyer willingness and user turnover rates, leading to a reduction of fee-earning transactions in the industry.

The key takeaway is the relationship between mortgage rates and the 10-year Treasury note. The spread between the two is currently enlarged, indicating a higher perceived risk of mortgage defaults. This implies that even if the Fed cuts rates again, mortgage rates might not fall proportionally, as lenders are pricing in additional risk.

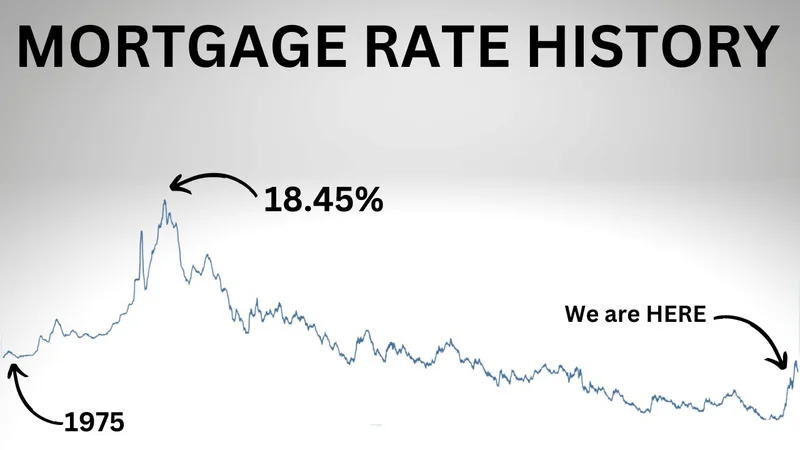

I've looked at dozens of these reports, and one thing always jumps out: the historical amnesia. Articles breathlessly compare today's rates to the rock-bottom levels of 2021 (2.65%!), conveniently omitting the fact that rates in the 70s, 80s, and 90s were significantly higher (exceeding 18% in the early 80s). Those rates were possible due to unprecedented government action aimed at preventing recession as the country grappled with a global pandemic.

The author of "Trending mortgage rates" correctly states that in the long term, property prices experienced today are undermined by high FRM rates over recent years. High mortgage rates translate into reduced ability to buy.

Navigating the Uncertainty

So, what's a prospective homebuyer to do? The advice is always the same: improve your credit score, lower your debt-to-income ratio, and shop around for the best rate. But let's be honest, those are table stakes. Everyone should be doing that. The real question is whether to jump in now or wait.

The answer, as always, depends on individual circumstances. If you can comfortably afford a mortgage at today's rates, and you plan to stay in the home for the long term, then waiting for a potentially lower rate might be a fool's errand. You could be waiting indefinitely.

However, if you're stretching your budget to the breaking point, and you're betting on rates dropping significantly in the near future, then you're playing a dangerous game. The risk of rates increasing is just as real as the possibility of them decreasing. Mortgage and refinance interest rates today, November 25, 2025: Lowest 30-year rate this year

Don't Bet the Farm on a Fed Miracle

It all boils down to risk tolerance and long-term planning. Don't get caught up in the daily noise. Zoom out, look at the bigger picture, and make a rational decision based on your own financial situation, not on the hopes of a Fed-induced miracle.

Related Articles

Crypto Market Faces Headwinds: Analyzing the Macro Signals Driving the Dip

Generated Title: Bitcoin's Silent Standoff: Why a Sideways Market Masks a Brewing Storm The chatter...

The Fed's Latest Rate Cut: What It *Really* Means for the Future of Innovation

The Federal Reserve is flying blind. That’s not my assessment. That’s the word on the street from ec...

Comcast's Stock Is Finally Paying the Price: Why It's Tanking and the Corporate Excuses You're Supposed to Believe

A Confession, Not a Notice So, Comcast’s stock took a little dip the other day. Wall Street gets the...

QQQ's Cash Flow Crisis: What's Happening?

QQQ's Afternoon Hiccup: Is Allsopp Right About the Overvaluation? The Invesco QQQ Trust ETF (QQQ), a...

NIO Stock: Its Trajectory & What's Next

NIO's Electric Dreams: Why This Isn't Just a Car, It's a Revolution NIO. The name itself hums with a...

The GameStop (GME) Phenomenon Returns: Decoding the Price Surge and the Reddit Uprising

It’s October 2025, and if you’re feeling a strange sense of déjà vu, you’re not alone. The `GME tick...